Twice in One Week! My Other New Stock

Plus how I find stock ideas and why I invest in growing businesses that lose money

Paging IT… Paging IT!

With so many businesses scrambling to get online during the pandemic, the next big customer service push will be digital. Every technical difficulty creates a headache for all involved. Because when tech fails, people get angry. And I’m definitely one of those people.

Just watch a few YouTube videos, or the iconic Office Space:

For example, the other day I was on a Google Meet and one of the attendees couldn’t get their volume to work. This might have been user error, but regardless those technical difficulties caused a 5-minute delay to the meeting and some awkward silence. Thus the need for companies tracking and fixing these potential technical difficulties, and thus the simple reason for my investment in PagerDuty (Ticker: PD).

See their Investor Presentation by clicking here.

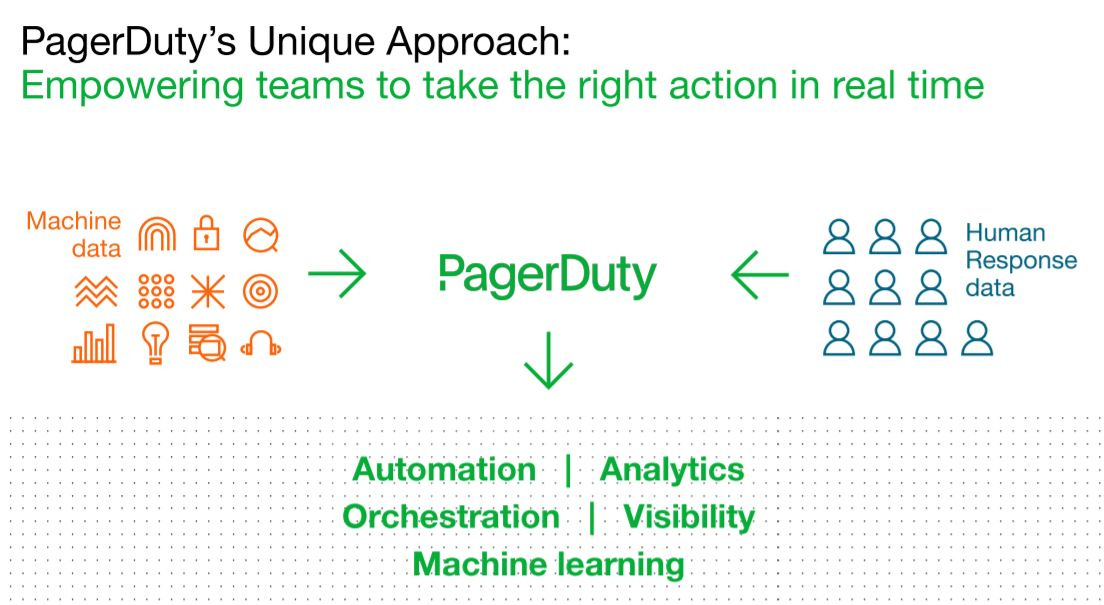

From PD’s investor relations page: “PD harnesses digital signals from virtually any software-enabled system or device, combines it with human response data, and orchestrates teams to take the right actions in real time. [Their] products help organizations improve operations, accelerate innovation, increase revenue, mitigate security risk, and deliver [a] great customer experience.”

On their conference call, PD shared three use cases for their software platform: (1) a grocery chain using PD for product recalls, (2) a utility company using PD to provide customers with outage information and service updates, and (3) a company providing electricity using PD to reduce manual processes that contribute to poor customer outcomes. These stories, along with their consistent innovation have led to some tremendous recent results.

Chairperson and CEO Jennifer Tejada opened her 4th quarter conference call with the following statement: “Through a combination of better macro conditions, secular tailwinds, like digital acceleration, cloud adoption, and DevOps transformation, and improved go-to-market execution, we ended fiscal '21 with $214 million in revenue, up 28% over last year.” The tailwinds for this platform are tremendous.

PD anticipates net retention of 118% to 124% (where current customers will spend 18% to 24% more than they did the previous year). On top of the net retention rate, PD has 85% gross margins (meaning each dollar of revenue they earned only cost them 0.15 cents to directly create) and incurred a net loss of only $6 million for the 4th quarter. With $560MM in cash on the balance sheet that also covers their debt, the company has a long runway to operate from a position of financial strength.

In terms of SAAS (software-as-a-service) valuation, PD is on the lower end of the range. Market cap is $3.6B, price-to-sales is 16 (nearly half of Twilio’s P/S ratio), and the price has appreciated only 104% over the last year. I chuckle at “appreciated only 104%” because that would be an amazing return over one year for any stock, but in retrospect PD was beaten down in 2019 prior to Covid shutdowns and the price appreciated much less than other SAAS companies.

Their addressable market also continues to expand as the need for digital emergency management and efficient online operations accelerates post-pandemic. I also believe this company could be a potential acquisition for someone like Twilio, Salesforce, Microsoft, Zoom, etc. looking to expand their suite of products/offerings.

Either way I think the potential for a nice return over the next 2-3 years or longer is in play with PagerDuty.

How I Find Investment Ideas

All Around Me

Watching YouTube videos recently, I began seeing people switch away from Monsters (Ticker: MNST) and pick up Celsius (Ticker: CELH). I thought this was odd, so I swung by my HEB and noticed the displays putting Celsius drinks front and center. Grabbed a couple, tried them, and haven’t stopped drinking them since.

Putting 2+2 together, this started me down the path to research and ultimately invest in CELH, especially since MNST has been one of the best performing stocks in history (crazy to think but check the stats).

Side Note: I have since sold my position in CELH to focus on concentrating in other investments I like better. CELH is just tapping the surface of possible expansion and product offerings, but they are also in a more challenging energy drink environment than MNST was in the early 2000s. It will be fun to see how the story plays out.

But back to my point… I find stock ideas all around me by watching YouTube, Netflix, etc… or walking through the shopping centers and noticing the busy shops/restaurants… or recognizing the items I purchase around the house constantly… or seeing the software packages that my company adds over time.

Podcasts

Any time I am accomplishing a mindless task, I listen to podcasts. It has made the drudgery of folding laundry infinitely more enjoyable (although still not anywhere close to enjoyable). Personally, I find the folding and then immediate unfolding of clothes to wear them the most pointless function in the history of functions. It’s a viscous, energy-sucking cycle. Sorry… end of rant.

Below is a list of my current podcast subscriptions:

Motley Fool Money

Market Foolery

Rule Breaker Investing

Motley Fool Answers

Industry Focus

Fast Money

Mad Money with Jim Cramer

We Study Billionaires

The Acquirer’s Podcast

The Razor’s Edge

The Business Brew

They help me gather stock ideas, understand trends/industries, and build my investing knowledge. Some I listen to every episode, and others I pick and choose. Overall, I have probably learned more from these podcasts than any other source.

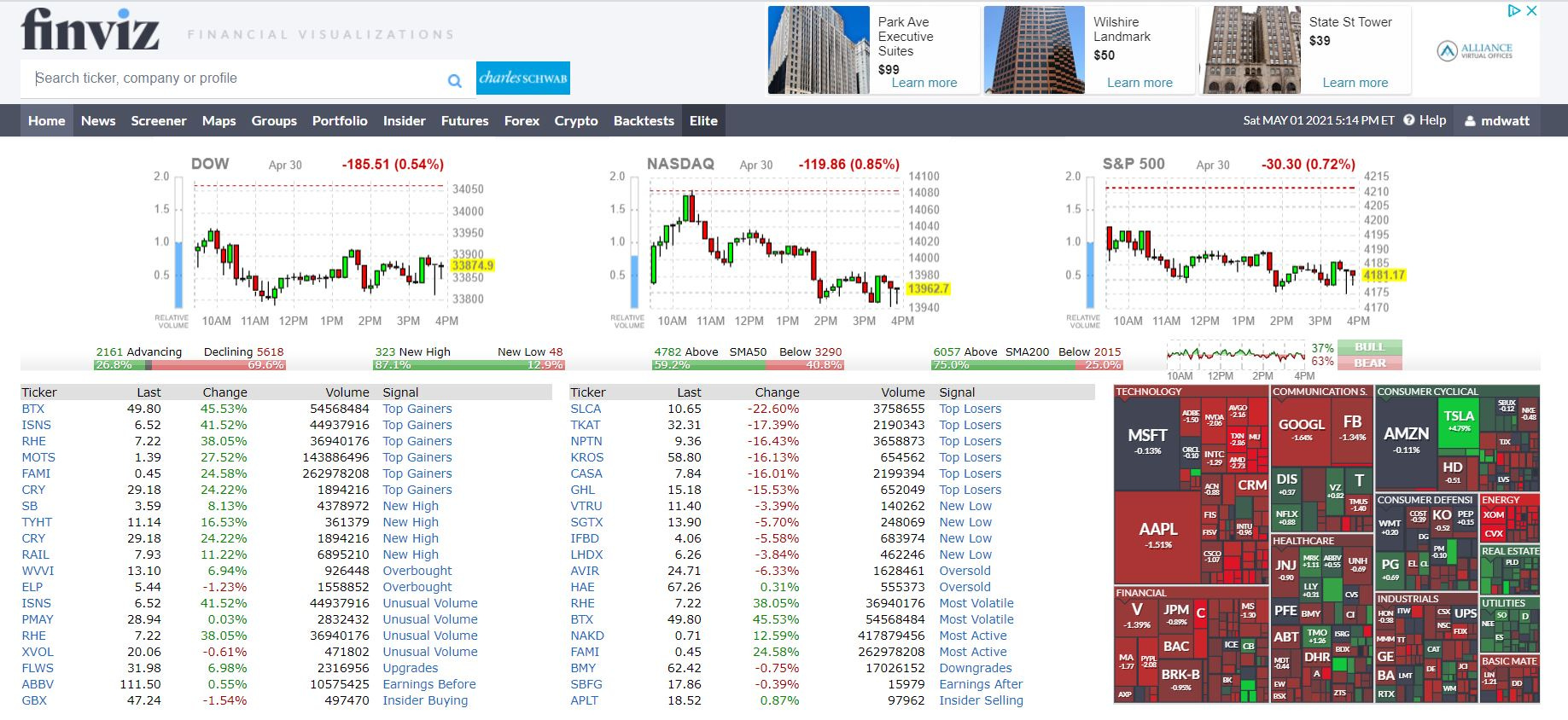

Finviz screener

I love playing around with Finviz.com’s screener tool. Add a few characteristics and it spits out a list of potential companies to research.

One of my favorite screens on Finviz is a breakout screener. I like to see stocks exhibiting strength and moving higher. It also gives me a look at what sectors/industries are on the move and could be a potential trend for the market. The screen is:

Market Cap -> +Small (over $300m)

Average Volume -> Over 500K

Price -> Over $5

Performance -> Quarter +30%

20-Day Simple Moving Average -> SMA20 above SMA 50

50-Day High/Low -> New High

Another screen I like helps me identify growing companies with strong fundamentals. The screen for that is:

Market Cap -> +Small (over $300m)

Average Volume -> Over 500K

Price -> Over $5

Sales growth past 5 years -> Over 20%

Current Ratio -> Over 1

Gross Margin -> Over 30%

Finviz also allows me to sort the results by a specific column. So sometimes I use the strong fundamentals screener, and then sort them by their Dividend % under the “Financial” tab.

Fintwit

Fintwit = Financial Twitter

Twitter has a wealth of Fintwit personalities. Some spew get-rich-quick schemes, but for the most part they share a wealth of amazing investment information. Like all things, don’t just follow the crowd for the heck of it. Use the crowd to gather ideas, research, and then make an informed decision for yourself. Hopefully just like you do with my newsletters.

If you want, follow me on Twitter @matt_invests. I retweet a lot of other Fintwit personalities that I respect and appreciate.

Conclusion: Bringing Together Multiple Sources

I start taking notice of a company when I see them in multiple searches. For instance, I used a screen toward the end of the summer 2020 that identified PagerDuty. I then saw Cathie Wood of ARK owned shares of the company (its never a bad thing if there is institutional or big money support). Finally I saw a Fintwit post from someone I respect on Twitter about the company that also referenced The Razor’ Edge podcast talking about PagerDuty. I listened to the podcast, researched the financials and the story, and read the most recent quarterly report. The company checked all my boxes and with the funds available in my account, I invested.

There is validation in having multiple sources identify an investment opportunity. So I make sure to take notice when it occurs.

Why I Invest in Growing Companies Losing Money

All companies start off as an idea (i.e. let’s try to make some extra money by renting out an air bed in our apartment). In order to turn that idea into a functioning business, it requires time and capital. The owners of the idea can put in their time, and largely their own capital in the early days (or family/friends capital), and get the idea up and running as a business. By the time the first person rents that air bed, a lot of time and capital has already gone into the business, thus creating unprofitability.

The new revenue will now bring more capital into the business in the form of cash. The business can enjoy the revenue of one air bed without incurring anymore expenses by renting it out over time and thus creating a profitable small business.

But in order for the business to expand to multiple air beds, or AirBnBs, they need consistent infusions of capital to keep up with the growth. The business owners might tap into their own wealth, but if they don’t have enough then they look to debt (loans) or investors (selling a percent of ownership in the business) to infuse capital into the company for growth/expansion.

At any snapshot in time, the business is unprofitable because the revenue they receive for their air beds is outpaced by their push to expand to new markets, thus driving more future revenue, but also incurring current losses.

At a certain point in time, the business should see revenue outpace expenses, finally creating a profitable business. Some companies are supported by debt and investments for a long time as they grow. For example, Amazon was consistently unprofitable until 2016.

I also highlighted AirBnB because it is one of those companies that is currently unprofitable but growing. And that’s the key: growing. If a company stops growing, then the debt and capital infusions stop, and the business will either need to cut costs/restructure, sell themselves, or potentially shut their doors. The goal for AirBnB is to become profitable, which I anticipate they will in the coming years. The confidence in my investment in AirBnB, even though they are currently losing a lot of money, stems from a few things:

Growth of revenue 30%+ the last two years before the pandemic. They also spent $2.7B on research and development in 2020 to continue innovating for the future.

On the conference call, ABNB stated they cut expenses during the pandemic that will never return, creating a quicker path to profitability.

They have $6.4B in cash on their balance sheet that would allow them to operate for ~10 more quarters if the pandemic was still in full swing (hopefully with the vaccine rollout we are winding down the pandemic).

Investing in unprofitable businesses does present more of a risk because they are reliant on capital infusions, but that also means the reward is that much greater by catching them before they obtain that profitability. Because they are growing, unprofitable, and thus more risky, I tend to rely heavily on strong management/operators because they are the ones making the decisions in the early days that will hopefully lead to future profitability.

Thank You!

If you’ve made it this far, then you are an amazing human. Let me know what you think by leaving a comment. Or drop me a question. Share it with others who you think might appreciate the information. Looking forward to sending out the next issue!

**I am not a financial advisor, so please don't buy/sell anything based solely on what you read here and do your own due diligence.