Our Plan to be Retire-able in 8 Years

Plus Updated Top Ten Holdings, Huge Investable Trends, and Q&A

Money is not the goal.

Money is a tool.

Freedom to choose is the goal.

How might your life be different if you could retire right now? What would you do? Would you be working at your current job? If you walked into your workplace today knowing that you could retire if you wanted, what stresses would be released from your psyche? Think of the possibilities.

Now Google search “retired” and click images. What do you see? I’ll wait a sec… I saw lots of pictures of couples with gray hair across my screen. That’s the idea of retirement… old and gray. But what if you could retire sooner, or more specifically in 8 years. What would it take to do that?

These questions and more drive my wife and I every day in our spending and investing decisions, and helped us put together a plan to be “retire-able” in 8 years (after 1 year we are still on track). I no longer feel the need to keep up with the f****** Jones’s. My wife and I still enjoy life. We have just prioritized our spending on the things that bring us the most joy, and focused on building wealth over the long term with quality/productive assets.

Here’s our plan:

Quick caveat before I begin. It took us quite a few years to get here. So this might be our current plan, but it definitely hasn’t been our only plan over the years.

(1) Live on less than 50% of our take home pay

Currently we are living on less than 40% of our take home pay. I don’t think this will continue after the pandemic ends, but we will still be under our goal of 50% or less. As a general rule of thumb for estimating retire-able years, I use the following breakdown that is based off of the 4% retirement rule and investing in the S&P 500 with 8% per year returns:

If you save 5% per year, then you can retire in 48 yrs with the same lifestyle.

If you save 10% per year, then you can retire in 39 yrs with the same lifestyle.

If you save 15% per year, then you can retire in 33 yrs with the same lifestyle.

If you save 20% per year, then you can retire in 29 yrs with the same lifestyle.

If you save 30% per year, then you can retire in 23 yrs with the same lifestyle.

If you save 40% per year, then you can retire in 18 yrs with the same lifestyle.

If you save 50% per year, then you can retire in 15 yrs with the same lifestyle.

If you save 60% per year, then you can retire in 11 yrs with the same lifestyle.

(2) Pay off the house by 1/1/28

By paying off the house prior to achieving “retire-ability” we will accomplish two things: (1) we will drastically lower our annual expenses and save interest expenses, and (2) we will have full ownership of an appreciating asset. We could rent it out and travel for a year or even use the cash flow to pay for another house.

Technically we could make more in the stock market than paying off the house, but the resulting peace of mind cannot be replaced. And the math isn’t too far off from the stock market. Houses have averaged 5% appreciation per year over the last 40 years and combined with the 4% interest we would save each year, then we would receive a not-too-shabby 9% return for those 20 years.

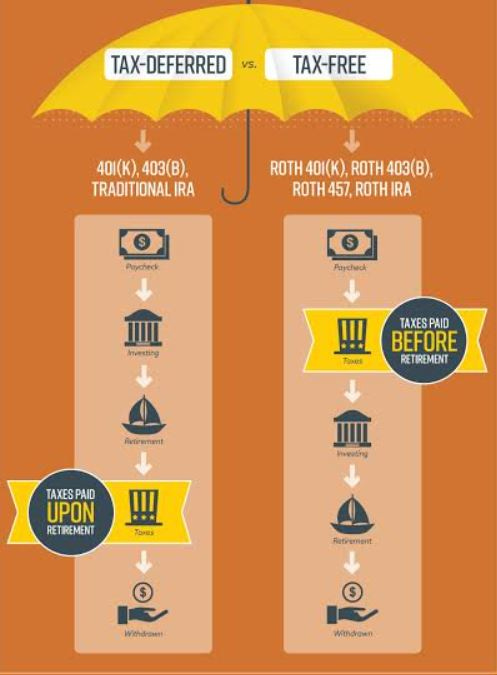

(3) Max out our IRA’s each year

An individual retirement account or IRA is one of the strongest vehicles for wealth creation available to us. As of 2020, we can put $6K in each of our accounts, invest the funds, and grow those funds tax free. There are more intricacies to the IRA, but this is the first vehicle we started using on our wealth building journey.

Side Note: You can research which IRA is right for you by clicking here.

(4) Build a 2-year emergency savings in cash to weather any market downturns.

The average market downturn of less than 20% takes an average of 4 months to recover. The average market downturn greater than 20% takes an average of 2 years to recover. In order to make sure our assets will have a chance to recover, we will have a cash balance to draw from so we don’t have to sell anything for that 4-month period or, in a worst case scenario, that 2-year period.

This is where we will use a high interest savings account to continue to accumulate cash and earn interest over the years. Of course the interest rates right now are a pitiful 0.5%, but before the market crashed in March 2020, they were at a much better 2.2% interest rate return per year.

(5) Invest in strong companies with excellent leadership for the long term.

After maxing out our IRAs, we also have a taxable brokerage account to increase our investment returns and be able to live off those assets prior to hitting age 59.5 when we can pull money out of our IRAs. In those accounts we want to invest in high quality companies.

Market pullbacks occur. Companies slip up. Over time, the cream of the crop will rise to the top. Picking high quality, productive companies with strong management will give us a leg up in compounding our investments. And the amazing thing is that we don’t even need to be right a majority of the time. Stocks have a cap on losing money at 100%, but they can growing infinitely.

(6) Increase our yearly incomes while avoiding lifestyle inflation.

My wife and I strive to be “so good at work that they can’t ignore us” (read the book So Good They Can’t Ignore You by Cal Newport for the reference). This can only help us when it comes time for raises, bonuses, or amazing opportunities with other companies.

Partaking in side hustles is another option. The possibilities are endless from selling on Etsy to creating an online business or even doing contract work on Fiverr.

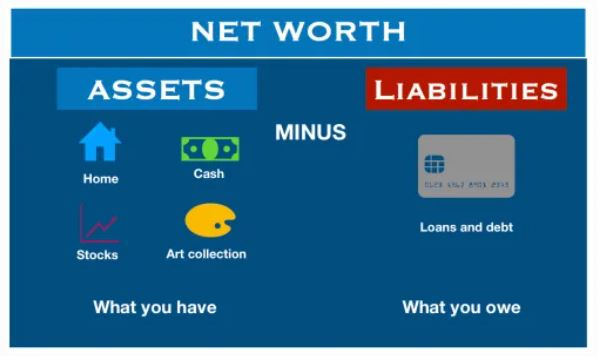

(7) Review our net worth and goals every two months.

It is not my wife’s favorite thing to sit down with me and understand our financial and investing plans, but once every two months keeps it to a reasonable level. In that hour long meeting, we get a chance to review our net worth, see the progress, and adjust the plan if necessary. Those 6 hours each year are probably the most impactful thing we can do for our future.

Side Note: Prior to this plan, I had to create a plan to get out of debt. It doesn’t matter where you are in your life, put together a plan and set dates to review it. It will drastically improve your chances of success. It has been statistically proven by many financial institutions (check out this Wealth Survey from Charles Schwab by clicking here).

Current Top 10 Holdings

PINS - Pinterest - 5.6%

DKNG - DraftKings - 5.1%

MELI - MercadoLibre - 4.8%

CHWY - Chewy Inc - 4.4%

CRLBF - Cresco Labs - 3.5%

GTBIF - Green Thumb Industries - 3.5%

TDOC - Teladoc Health - 3.3%

CRWD - Crowdstrike - 3.2%

RDFN - Redfin - 3.1%

TIGR - Up Fintech Holdings - 3.0%

Just Missed: PRCH, GDRX, PTON, THCB, SE

Over the past few weeks I have been solidifying my portfolio investment thesis and management plan. My goal is to have a portfolio in the millions of $, so even though I might not be there yet, I want to plan as if I am. I will write a future newsletter about these changes. Stay tuned.

What Trends Am I Currently Watching?

Electric Vehicles - Cars, commercial vehicles, batteries, rare earth metals, support services

Cannabis - MSOs, online services, products

Sports betting - Online operations

Space - Any and everything aerial

Fintech - Helping the unbanked

Healthcare digitization - Telehealth, solving price inefficiency, chronic care, wearables

E-commerce - All of it.

Advertising tech - Mobile advertising, connected TV advertising

Genomics - Just now learning, but might be the most important industry in the next 10 years outside of maybe Space.

Q&A

Q: How do you budget?

First off, if you have never budgeted before or created a monthly budget, then pick up The Total Money Makeover by Dave Ramsey. Start there.

I have used his system, but over time have developed my own flexible budgeting plan that prioritizes my spending. This is what I do:

Step 1: I list out my budget items for the month and the amount they cost. This is everything from the house to the car to clothes to fun-tivities and everything else in between (after the first time it gets easier because you only have to add the fringe items like an oil change that occur every few months or once a year).

Step 2: I rank each item from the most important to the least important for the month.

Step 3: I then add up the amount of money I have coming in my accounts for the month.

Step 4: From that money, I subtract out the amounts that I want to invest and save.

Step 5: With the remaining money, I go to my budget items and I begin subtracting out each item in order. Once I hit $0 left, any remaining budget items are removed from my budget for the month because I can’t afford them. So this might be clothes that I wanted to buy, or a haircut that needs to be delayed until the next month.

Step 6: I finish by making any adjustments. Maybe I can eliminate one night out and get one outfit of clothes rather than the three outfits I was planning.

Step 7: Begin again each month. Steadily over time this becomes second nature in your decision making.

A budget can be helpful to manage monthly finances, but in the end there is only so much you can cut from a budget. The best thing you can do for yourself (something I did for myself by switching careers) is to strive to increase the money coming into your accounts. If you are at this point, then a helpful read would be Ramit Sethi’s I Will Teach You To Be Rich. Definitely hone in on his section about increasing your income.

Find the right budget that works for you and stick to it. It only works if you do.

Thank You!

If you’ve made it this far, then you are an amazing human. Let me know what you think by leaving a comment. Or drop me a question. Share it with others who you think might appreciate the information. Looking forward to sending out the next issue!

**I am not a financial advisor, so please don't buy/sell anything based solely on what you read here and do your own due diligence.